[Reading time: 4 minutes]

I have two friends (now clients) - Nishant and Kshitij (names changed). Recently, we got into an argument about renting v/s buying a house.

And while I was of the opinion that Nishant should buy one (Yes, I recommended BUYING a house), I told Kshitij that he should rent one, even though they both earn more or less the same income and are the same age.

Because, here’s the thing.

Both have very different backgrounds, mindsets and situations.

So today, we’ll talk about what you should consider and how you should decide whether or not to buy a house. And in 3.5 minutes from now, you’ll not just be a pro at this yourself, but will also be able to help out your friends take this decision 😉

Chalo, let’s look at Nishant’s case: He’s 33 years old, a software engineer earning about 2.5 lakhs per month, stays in Hyderabad and has a 3-yr old baby. He invests primarily in low-risk products, and has about 20 lakhs that he can use for down-payment if he wants to buy a house.

Now, here’s how you can objectively decide whether to rent or to buy:

→ Quantitative factors: You first consider the financials. Note down these numbers:

Rent of the property v/s buying cost of the same property

Yearly increase in rent v/s Yearly Real Estate price appreciation for the same property

Down payment amount and interest rate, if you take a loan

Lastly, in our country, there will always be a difference between EMI and rent (EMI for the same house will be higher than rent paid). So the money that you’re saving by renting, will you invest it? And if yes, where? Note that down.

Once that is done, you put these values in a Rent v/s Buy calculator (link at the end of the article) and check your net worth, in both cases.

You just need to input these values, and the calculator will consider all these parameters and tell you your net worth, and subsequently what makes better financial sense for you.

Once you see what makes sense financially, you then look at Qualitative factors:

Will the real estate market appreciate in the city you stay in?

Do you need location stability right now?

Is buying a house an emotional/aspirational decision?

In Nishant’s case,

He stays in the suburbs of Hyderabad, where real estate prices are not very high, and there is still scope for price appreciation

He has a baby who will be going to school in the next 2 years, so location stability will be helpful

He is risk-averse and invests in very low risk products. So financially, the money he’d save by paying rent instead of EMI, will not give him a very high return.

If you put these numbers in a calculator, you’ll see that Nishant will actually benefit by 4 CRORES if he buys his house instead of renting it.

So for him, buying is the way to go!

Now, let’s move to Kshitij. His situation is different - He stays in Mumbai, earns about 3 lakhs per month, invests in equity and is unmarried (I still haven’t understood what he does for a living though - he’s the Chandler/Barney of the group 😉).

But in his case, renting makes more sense, because:

Real Estate prices in Mumbai are really really high, with very low appreciation possibilities

He’s a free bird. He’s in Mumbai right now, but was in Bangalore before this, and may move again to another city if he gets another job. He’s not married, and doesn’t intend to either (he could probably be in Argentina next year, for all I know 😛)

Most importantly, as an investor, he has a high risk appetite, which means he also has a probability to earn higher returns. So if he rents his house instead of buying it, he’ll save a lot of down-payment money which he can invest. And the difference between EMI and rent also could be invested in an SIP and get him good returns

Which is why, in Kshitij’s case, it makes more sense to rent rather than buy.

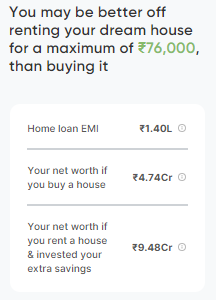

Nishant and Kshitij’s scenarios:

Below are the calculated values for both Nishant and Kshitij, after they use the calculator:

Nishant’s scenario (after inputs)

Kshitij’s scenario (after inputs)

You see, renting v/s buying is not a decision you can generalize. You need to first see if you’re buying it from an emotional/aspirational perspective or a financial perspective. If it’s aspirational, then as long as it doesn’t screw your financial health, go ahead. But you NEED to consider the financials, even if it’s more of an emotional/aspirational decision.

Calculator:

Fi, a neo-banking startup, has a pretty good calculator that you can use to check this from a financial perspective. Play around with the numbers and see for yourself HERE

Well, that’s all for today! I’m sure this will help you arrive at a decision whenever you intend to buy a house.

If you have any queries, feel free to comment or write back to me, and I’ll respond ASAP 😁

Till next week, adios! Have a lovely Sunday!