Ever wondered why credit cards are free?

Well, banks earn from free cards too!

[Reading time: 4 minutes]

Before we begin, there’s just one week left to file your taxes! So if you haven’t done it yet and need help, reach out to us HERE and we’ll connect you with a CA who will help out.

Now, let’s begin.

So, 10 years ago when I started using credit cards, I always used to wonder - How the hell can these banks give me a credit card and not charge me a penny for it?

If you’ve ever wondered about this, read on to know how that’s actually possible.

To understand this, first you’ll need to understand what happens at the back-end when you swipe your credit card at a store. Just stay with me for the next 4 minutes, and you’ll get this whole thing.

So just re-imagine the last card swipe transaction you did, and think about how your card looks.

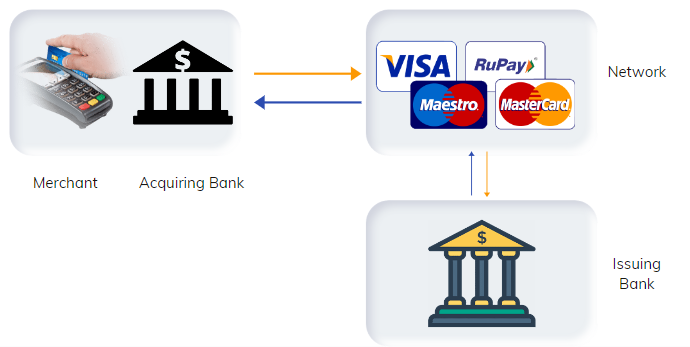

Your card will have the logo of Visa, Mastercard, Rupay or something like that. This is known as the card network. Basically card networks issue cards along with banks. So if you have a Visa ICICI credit card, it’ll be issued by Visa along with ICICI Bank (known as the Issuing Bank).

Now when you swipe your card, just try to remember the card swipe machine. Most probably, it will have a bank’s name written on it somewhere (in certain cases, it may be another company’s name which is not a bank, but for now, let’s just ignore that). Let’s assume that this is SBI. This bank is known as the Acquiring Bank. Which means that your ICICI card is swiped on the machine of SBI.

(There are 3 new terms you learnt till here - Card Network, Issuing Bank and Acquiring Bank)

Now, SBI doesn’t know who the owner of the card is. Heck, it doesn’t even know which bank has issued this card. SBI just knows that this card is issued by Visa (which is determined by the first 2-6 digits of the credit card number (known as the Bank Identification Number, or BIN). So SBI reads the BIN and sends this transaction details to Visa.

(Again, this routing system known as the SWITCH, can also be developed by another company which is not the acquiring bank, but let’s leave that for now, to keep it simple. We’ll just assume that SBI has done it)

Coming back. From the BIN, Visa knows which bank has issued this card (because duh, Visa has only worked with the bank to issue it, right?).

So Visa knows that boss, this is an ICICI Bank card. Now Visa will send these transaction details to ICICI Bank, saying “Bro this particular card number has been swiped at some shop. Just check and tell me if this card has sufficient credit limit”.

If there’s sufficient credit limit, ICICI tells Visa to proceed ahead with the transaction. Visa then sends this confirmation to SBI, and the SBI machine then tells you that your transaction is approved. ICICI Bank now reduces your remaining credit limit (and increases your bill 😛).

And all of this happens in less than 5 seconds. Yayyy Fintech! 😎

Here’s a pictorial representation of all of this:

Okay, now suppose you swiped this card at, say, Big Bazaar (BB). Now, BB does not get the money immediately. BB basically has a current account with SBI. So first, ICICI Bank pays Visa, who then pays SBI, and SBI then credit’s BB’s bank account. This generally happens on the next day of the transaction.

Okay, phew! Now that you know how a card swipe transaction actually works, let’s see how banks make money on credit cards, shall we?

Uh uh..before that, if you’re not subscribed to this newsletter, why don’t you do it before moving ahead? 😁

Okay now let’s take a hypothetical example. You bought Maggi and Pepsi at BB, totalling Rs. 100. Now you swiped your card, and your transaction was approved (after all the hops that we discussed). Now, BB will not get the entire 100 bucks in its account. It’ll get 1-3% lesser. Whether it’s 1%, 1.5% or 2%, depends on the agreement between BB and SBI, so let’s not get into that. Let’s just assume that the BB guy was a pathetic negotiator and he ended up agreeing on a 2% share.

This 2% is known as the Merchant Discount Rate (MDR). As the name suggests, it’s the discount that the merchant (BB) bears for the transaction.

This 2% (or 2 rupees in our case) is distributed to primarily 3 entities - SBI, ICICI and Visa. The major chunk of it goes to the issuer bank (ICICI Bank in our case) and the remaining is split between other entities.

And THAT, my friends, is how your bank makes money on your credit card, and can afford to give you a lifetime free credit card. It doesn’t earn from you, but earns from the seller. The share of the MDR that goes to the card issuing bank is known as the Interchange Income.

“Why does the merchant (seller) have to bear this MDR”, you ask?

Well, because the merchant is getting another mode of payment and convenience that it can offer to its customers. This is why, earlier, merchants were reluctant to accept credit cards. Because it eats into their profits.

But after Modiji’s grand slam of demonetization, they didn’t have an option, and HAD to offer another mode of payment. Slowly, card payments caught on and now it’s considered as a must-have for any merchant. Poor guys 😞

Now, Interchange Income forms one part of the income for the issuing bank. They make a lot of money from late fees and interest charges too when people miss their payments or pay only the minimum amount due. But yeah, the more you spend on your credit card, the more your bank earns from interchange 😁

And that’s how it’s done, guys!

Do like this article if you made it till the end, so that I’l know it was helpful. Or you can just send me an email saying it helped🙂

PS: There’s just one week left to file your taxes! If you need assistance with it, please feel free to get in touch with us HERE, and I’ll connect you to a CA.

Nice and interesting read! Which are these other companies that can also develop SWITCH and which are not the acquiring bank? What are they called, how does it work and do they need to have some acquiring bank at the backend to complete this transaction flow?

took me 6 min